Why Picking the Right Fund Manager Matters More in Private Markets

Lately, everyone I talk to wants a piece of private markets. They want to own the latest shiny AI or quick commerce startup. They need a “startup portfolio” for dinner party conversation. They have dabbled in public markets — some successfully.

Most made their money in other sectors — manufacturing, pharma, consumer goods. The second gen, returning after studying abroad, does not want to “run” the family business. They would rather do strategy, manage money, corporate development. The cool stuff.

They are just getting started. Still learning to deploy capital. The world is their oyster — mutual funds, stocks, debt, real estate, gold, private markets. Easiest to fall back on wealth advisors or the structure the first generation built. But therein lies the fallacy.

A CEO of an asset management firm recently told me: “An investor is an investor in all asset classes. What do you mean you do not invest in public markets?” On the surface, he is right. But I believe specialisation exists. The same investors who quote Buffett on long-term compounding forget he also said: “You have to know what you understand and what you don’t understand. It’s not terribly important how big the circle is. But it is terribly important that you know where the perimeter is.”

I believe a VC investor cannot do PE. A PE investor cannot do public markets. A public market investor cannot do real estate. and vice versa. You get the drift.

Actually, scratch that. An investor can invest across asset classes — they will just not be the best. To be top decile, you need specialisation. Maybe a handful of people can be exceptional across asset classes.

The dispersion of top-decile returns increases as you move from real estate to mutual funds to public markets to PE to growth to early-stage investing.

That is the central thesis of this piece. I hope to convince you of the same.

I dug into Indian mutual fund performance data. Of 842 schemes, 485 carry a full three-year track record. I looked at only three year data, because average MF holding is 2.5-3 years.

If you were to guess, how many would you think hit top decile?

The cutoff: 24.7% 3-year CAGR. Top quartile required 19.2%. Median sat at 17.8%. The gap between top decile median (26.6%) and bottom decile median (10.6%): 16 percentage points.

Those 49 top-decile funds come from 26 of the 44 registered fund houses. Top quartile spans 30 houses. That means roughly two-thirds of India’s mutual fund houses had a top-decile scheme.

Throw a stone in the mutual fund market and you have a pretty good chance it hits a top-decile manager.

Now pick a random fund from the 485. How bad does it get? The gap between top decile median and overall median is 8.8%. You underperform by a few points. You redeem. You move on.

For the average mutual fund investor, 49 funds is like going to a 5-star hotel for a buffet - you have a large spread of really good food to choose from. Eat all you want!

Step up to Indian PMS funds. Analysis of 521 PMS strategies on PMS Bazaar found 40% beat the Nifty 50 and 15% beat the Nifty Midcap 50. Top-quartile PMS returns: 20-25% CAGR. The bottom quartile? A January 2026 rout pulled the average PMS fund down 4.19% to the Nifty 50.

Finding a top-decile PMS manager is harder than finding a top-decile mutual fund manager.

Now try Indian venture capital. The Preqin-IVCA benchmark (748 schemes) shows VC has the highest median net IRR among all AIF categories — but dispersion is extreme. Top-quartile funds target 3.0x+ TVPI. Median funds return 1.5-1.8x. The bottom quartile destroys capital entirely.

How many funds hit top decile? Maybe a handful.

I believe the distance between top-decile and median performance increases at every step from public to private to early-stage. The fuzzier the asset class, the more it matters who makes the bets. In public markets, picking the wrong fund manager costs you a few percentage points. In private markets, it costs you the entire vintage.

This is not a marginal decision. It is the decision.

Why this happens

Seth Klarman has a useful framing. In public markets, fund managers manage inventory. Stocks are liquid, replaceable, priced in real time. A bad pick gets sold. The cost is a few points. Manager skill operates at the margin.

In private markets, fund managers build assets. Each company is a multi-year bet with binary outcomes. A bad pick cannot be sold at market price. It sits on the books until it exits or dies. A single position can drive fund returns i.e. what’s called Power Law or Price’s Law.

The compression thesis explains the gap: Technology compresses information asymmetry in public markets. Bloomberg terminals, real-time pricing — everyone sees the same data. In private markets, technology compresses nothing. Company performance stays opaque. Manager skill cannot be proxied by a ticker symbol. The less the market tells you, the more the manager matters.

Why It Matters

A bad public market fund trails the index by maybe 200 bps. You notice it in a quarter. You fire the manager. Liquidity is your escape hatch.

Private markets offer no escape hatch. A bad VC fund selection means capital locked for 10+ years with near-zero return. No redemption window. No secondary market without a 40-60% haircut. That leaves a bad aftertaste — and makes it harder for that LP to trust and invest in other managers.

Every rupee flowing into private markets needs a manager on the other end. LPs making allocation decisions. Fund-of-funds managers. Family offices entering alternatives. HNIs allocating to PMS and AIF strategies. Founders choosing investors. The asymmetry is built into the structure.

Supporting Evidence

What LPs Actually Prioritise

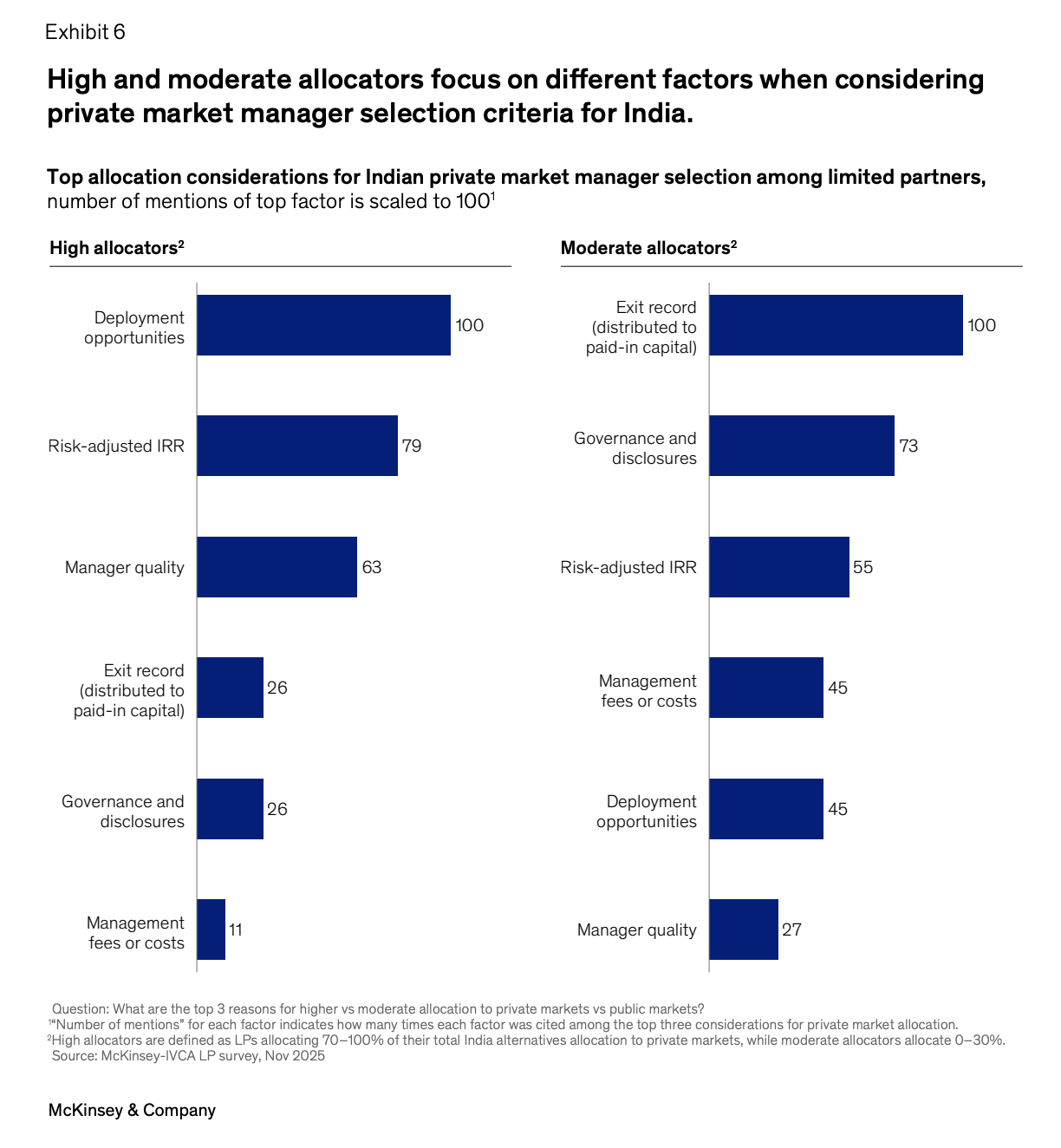

The McKinsey-IVCA LP survey (November 2025) asked global LPs to rank GP selection criteria for India. Top of the list — no surprises — outcomes. Performance record (IRR) scored 100 mentions scaled. Exit record (DPI): 85.

Manager quality scored 63 among high allocators — and 27 among moderate allocators. When asked to rate Indian GPs, LPs gave every factor between 4.9 and 5.8 out of 10.

But the distribution bars tell a deeper story. The variation is wide. Some rate Indian GPs 8-9/10. Others give 2-3/10. LP opinion itself is dispersed.

This is the paradox. LPs pick on past outcomes — IRR, DPI, deployment. In an asset class where outcomes follow a power law, picking on past outcomes is driving by the rearview mirror.

But you can’t blame an LP for thinking this way. It’s how they pick wealth advisors, it’s how they pick PMS managers, it’s how they pick and evaluate how to deploy their money in the public markets. Why would they look at private manager deployment any different?

The public markets offers the same set of 3,000-4,000 companies to pick from, everyone gets the same information, everyone knows the same trading strategies, everyone gets the same disclosed information. What’s the difference? None, other than past returns.

Private markets behaves very different though. There’s significant information assymetry. Sometimes investment opportunities don’t even reach the market. Investors whose job it is to identify early stage investment opportunities, don’t even know a deal is happening, but a fund will pre-empt a deal and do it within their network.

That’s serious alpha that could drive fund returns. Picking that manager who gets access to that investment opportunity is everything. No LP would want to be invested with a fund manager who didn’t know that deal was in the making. Fund manager matters.

The Dispersion Ladder

Each step down the liquidity ladder increases the importance of manager skill.

Public markets: Of 485 ranked schemes, 49 hit top-decile (floor 24.7% CAGR). Bottom decile ranges from 2.9% to 11.1%. The gap between D1 and D10 median is 16pp. Across large-cap funds, top-to-bottom quartile dispersion hovers around 1.5pp — you can pick blind and stay close.

Caveat: Sectoral and thematic funds (PSU, infra, pharma) dominate the top decile partly due to cycle timing. But compare like with like — top quartile mid-cap funds still beat the bottom quartile by a wide margin.

Indian PMS: 521 strategies tracked. Only 40% beat Nifty 50. Just 15% beat Nifty Midcap 50. A 2024 study found PMS funds outperformed benchmarks by 61 bps per month on average — but that average masks extreme variance across managers.

Indian VC: Preqin-IVCA benchmark (748 schemes). Top-quartile early-stage VC runs ~30% net IRR. Median sits at ~14%. Top-quartile returns 3.0x+ TVPI vs median 1.5-1.8x. In a power-law asset class, this is binary: right fund or wrong fund.

Global PE sits between: 12.9pp dispersion between top and bottom quartile. The difference between a great PE fund and a bad one is not a few points — it is a full venture return cycle.

What Distinguishes Top-Decile Managers

This is a topic I think about a lot. I’m constantly learning on this. But I believe the three things i look for, are as below:

- Allocation access: The best managers get into the best deals before they close. That access attracts more capital. More capital secures more allocations. Circular? Yes. That is the point. Circularity is the moat. The question is not “Does this manager pick good companies?” It is “Does this manager get into the best deals before they close?”

- High conviction concentration: Top-decile Indian mutual funds hold 25-35 stocks versus the industry average of over 50 (Ventura Securities, 2026). The same pattern recurs in VC. Top-decile managers make fewer bets, larger commitments. They do not diversify away their edge. This is measurable, verifiable. Most claims of “conviction” are marketing; portfolio concentration is data.

- Bias for action: I think this applies for the best people in any field. The best people waste no time overthinking, they just act. They respond quickly, they decide quickly and they attract similar talent to work alongside them. The best fund managers are constantly networking and constantly sourcing opportunities. They’re a delight to watch operate.

Implications

For LPs and institutional investors: You are picking on IRR — the least predictive metric in a power-law asset class. The manager is the deployment opportunity. Here are three more predictive leading indicators:

-

Deal-flow rank: Where does this firm sit in the allocation hierarchy for the best 5-6 deals in its vintage? If they get cut from oversubscribed rounds, they are not top-decile regardless of past IRR.

-

Concentration ratio: What is the average position size as a percentage of fund? Top-decile managers concentrate. If the portfolio has 40+ positions, the manager is diversifying away their edge.

-

Fund size discipline: Has the manager capped or increased fund size? AUM growth in a finite deployment environment dilutes returns. The best managers cap their funds. The best LPs reward them for it.

Caveat: The McKinsey survey covers LPs allocating to funds above $100M. For larger vehicles the dispersion problem is less acute. The real alpha sits in identifying emerging managers before they cross that threshold.

For fund-of-funds managers: Your value proposition is not diversification. It is selection. If you cannot demonstrate a systematic edge in identifying top-decile managers, your fees are unjustified. The market will figure this out.

For founders: The VC you pick is the VC you are married to. A top-decile VC brings signal, network, follow-on access. A median VC brings capital. Diligence your investors as hard as they diligence you. Ask about their allocation access and conviction concentration. Ask about their last three passes — and why they made them.

Second-order effect: As more capital chases fewer top-decile managers, the gap will widen further. The best funds become harder to access. Cherry-picking is not naive. It is the only rational strategy.

Conclusion

The less liquid the asset class, the more manager skill determines outcomes. The dispersion ladder — from public markets to PE to early-stage VC — shows each step increases the gap between the best and the rest. In early-stage VC, the gap is a chasm.

Most LPs I know spend more time negotiating management fees than evaluating deal-flow access. They optimise for the 2% and ignore the variable that determines whether the 20% ever materialises.

The irony is that the information you need to pick correctly is available — concentration ratios, co-investor references, allocation history. It just requires different work than reading a deck. In an asset class where the manager is the return, that work is the only work worth doing.

Choose accordingly.